The national debt has been a pivotal issue in British politics. In 2010 and 2015 controlling our national debt was a key part of the Conservative message that helped deliver them victory but despite our national debt being higher than it was post-recession, its size does not concern most serious economists.

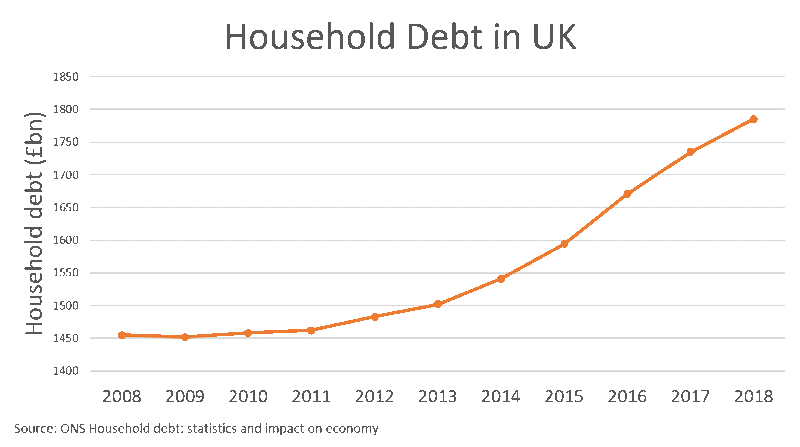

The debt that does is this nation’s household debt, the debt held by regular people like you and me. Household debt has risen dramatically in the last few years, fuelled by the enduring hardship created by austerity and should this debt bubble burst we would witness serious economic consequences. So why do we never hear about the substantial debt on our citizens? It doesn’t affect the wealthy of course.

The national debt has always garnered interest from our political class and now that our deficit has almost reached zero it may begin to fall unless Boris opens the taps on spending. However, the drastic economic consequences of austerity have pushed up another debt, our own. The reduced spending on services that we need alongside falling wages have meant British citizens have been pushed into more and more borrowing. In fact, Brits now find their finances in deficit for the first time in 40 years. In 2017, households took out nearly £80 billion in loans but they deposited just £37 billion with UK banks, an economic situation that ratings agency Standard & Poor’s label unsustainable and should raise “red flags”. The situation has got worse since that data was gathererd.

The picture gets worse when we consider unsecured lending has increased to record levels. This is short term debt such as credit card debt and overdrafts rather than debt such as mortgages and is even more volatile than other forms of debt. In short, we are one of the worst debtors in Western Europe.

This dramatic rise is most likely caused by austerity and the government’s reduction of the deficit, though the post referendum stagnating wages and rise in inflation have also spurred on the level of debt. The relation with public and private debt is one that is of increasing interest to Post-Keynesian economists especially those who put their faith in Modern Monetary Theory. MMT would suggest the dropping government deficit is pushing the rest of us into deficit but the way the government has gone about this may be a bigger reason for the substantial rise in debt.

Whatever the cause the rising debt has economic repercussions. Consumer spending is a vital part of our economy and while debt can help fuel spending in our economy, predictably those with higher debt also limit their spending and in our post-crash economy the impact of household debt has been to hurt growth via the limitation of spending. Equally the possibility of this debt has to cause serious problems in our economy should not be underestimated. If you want to know what happens when a bubble of debt burst research the 2008 financial crash. Credit can benefit the economy but always has risk and this level of it presents a threat to our economy.

We should ask serious questions of how our economy would fare in a recession caused by another factor that we may be heading into to. Wages have only just recovered from the crash of 2008 and with household debt at record levels, we are in a much worse place than we were when the global financial crash struck in 2008. Make no mistake the large household debt that hangs over us has an unrealised detrimental effect on society.

The cost for our persons has become severe, in a society obsessed with money. One in three people regularly worry about money to the extent that it has a negative impact on their mental health. Debt often triggers anxiety or depression. 9.5 million Brits have mental health issues as a direct result of financial anxiety. Our obsession with money and spending is destroying our personal lives and mental health, as well as the environment around us.

Debt also provides a deeper challenge to society, in both its welfare and liberty. According to philosophers like Lazzarato and Goodchild debt greatly reduces liberty and by binding us to the will of credit.

Lazzarato saw debt as the power behind all economic decisions, that we have become trapped in an ever-expanding debt bubble as profit is motivated by paying interest on loans. “Finance sees to it that the only choices and the only decisions are those of the tautology of money-making money, of production for the sake of production.”

In fact, due to money’s nature as purely credit, all these loans do is create money. Banks have the power to create money ex nihilo for loans. All persons, businesses and governments are enslaved to an increasing spiral of debt. This ever-growing spiral is needed to stimulate supply and the interest provides the motivation for businesses to pursue profits to service their loans.

In a wider economic sense, this means that this dramatic rise in household debt greatly damages the liberty of citizens through the need to pay their debts in a sense trapping them in poverty and servitude. Therefore, elimination of this debt should be a priority of parties across the political spectrum, whether they seek to maximise welfare or liberty, yet neither party has substantial policies designed to address it.

A version of this article was originally published by The London Economic